INSIGHT

02.19

When Margin Moves Under Refinancing

Reconstructing the Acceptance Record of an Operating Asset Under Refinancing

On a large-scale power generation program, mechanical completion and commissioning had concluded and the facility was operating within expected technical parameters. As refinancing discussions began, capital review extended beyond performance metrics and forecast margin reflected a 2.7 percentage point movement despite no deterioration in output or delivery execution.

The shift did not originate in operational performance. Attention turned instead to the record of delegated acceptance decisions exercised during execution.

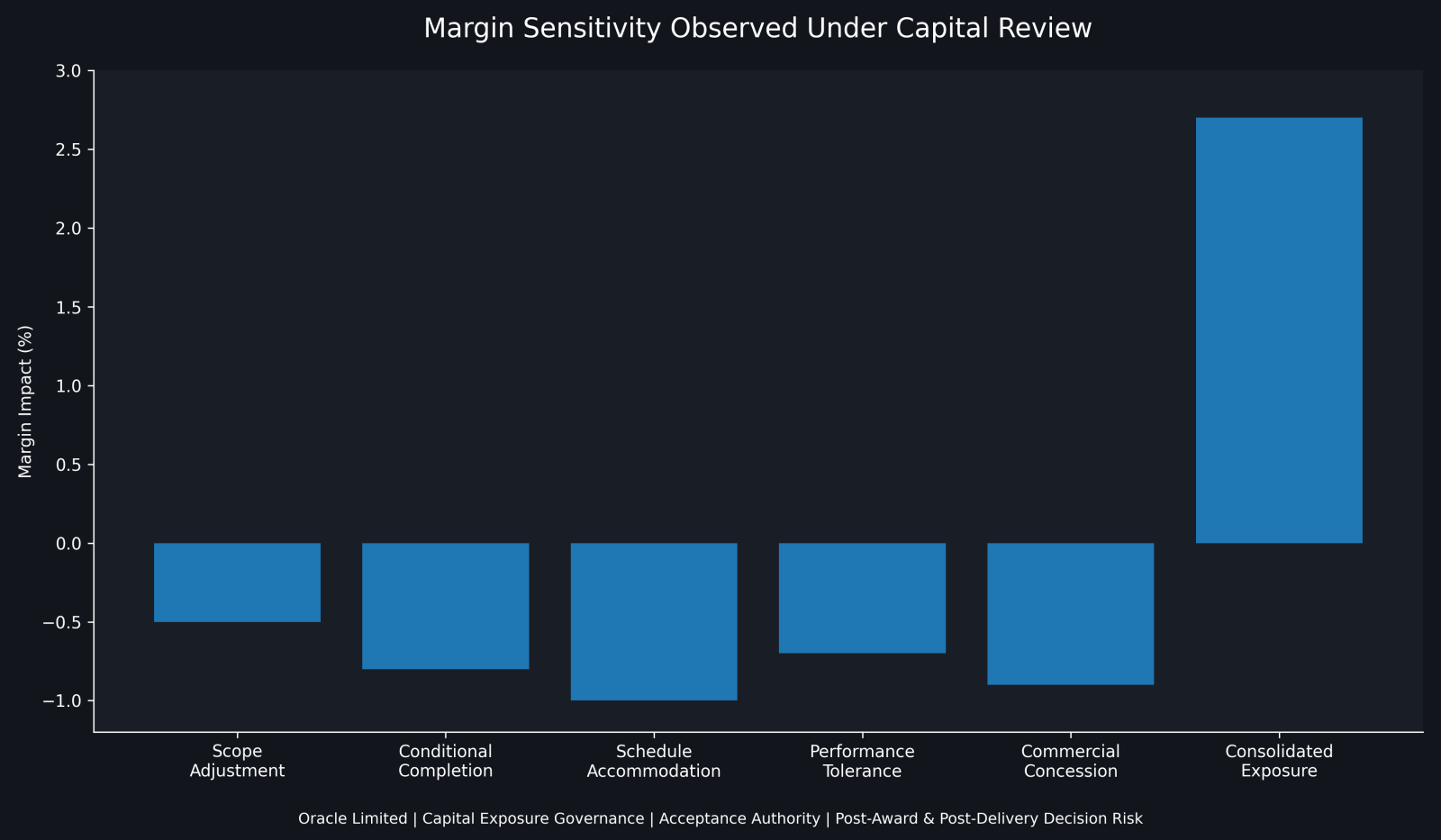

Those decisions included conditional completions, deferred scope items, schedule accommodations, and commercial concessions that had each been granted within defined delegation limits and supported by documentation. Individually, they were compliant. What had not been evaluated was their cumulative financial sensitivity when assessed collectively against consolidated margin thresholds.

Across reporting cycles, incremental approvals accumulated while package-level compliance masked aggregated exposure. When the acceptance record was reconstructed against defined authority boundaries, embedded financial sensitivity became visible within the margin forecast.

During reconstruction, acceptance decisions were consolidated across workstreams and evaluated collectively against cumulative contractual limits and defined margin sensitivity thresholds. Delegation boundaries were clarified and the full decision trail was reassembled, bringing visibility to the embedded financial effect of previously isolated approvals.

Once reconstructed and assessed in aggregate, forecast margin recalibrated from 9.4 percent to 12.1 percent. The 2.7 percentage point variance represented approximately $13.5 million in financial sensitivity that had been structurally embedded within compliant but unaggregated acceptance decisions. The asset had been performing as expected. The exposure sat within the consolidation of delegated authority rather than within operational execution.

Under capital review, valuation extends beyond production metrics and delivery performance. Historical acceptance decisions, conditional approvals, and delegated concessions influence how lenders, insurers, counterparties, and future owners assess financial durability. When ownership context shifts or refinancing begins, those decisions become financial evidence. Acceptance authority that is fragmented or insufficiently consolidated introduces valuation uncertainty even where technical delivery remains stable.

Structured consolidation of acceptance authority restored confidence in forecast margin and reduced exposure under capital, lender, and regulatory scrutiny. By aligning delegated approvals with defined margin sensitivity thresholds and reconstructing the decision trail in full, the asset’s financial position could be evaluated on transparent and defensible terms.

In capital-intensive environments, margin resilience is not governed solely by execution performance. It is shaped by how acceptance decisions are structured, aggregated, and preserved over time. Where delegated authority is exercised without cumulative sensitivity mapping, exposure can remain latent until financial review requires reconstruction. When authority boundaries are defined, consolidated, and traceable, margin position remains defensible under scrutiny.

—

About the Architecture

The Capital-Bound Authority Architecture (CB-AA) examines how discretionary authority exercised during delivery becomes financially consequential when capital scrutiny accelerates.

Explore the architecture:

Execution Margin Formation

Capital Exposure Reconstruction

Governance Instruments

—

Oracle Limited