Capital-Bound Authority Architecture (CB-AA)

Across Execution, Delivery, and Capital Examination

Applied across capital projects, regulated delivery environments, and institutional capital review.

Institutional capital projects generate thousands of discretionary decisions during delivery. When authority conditions surrounding those decisions are not structurally preserved, exposure only becomes visible later during lender review, audit reconstruction, or insurance examination.

Capital-Bound Authority Architecture (CB-AA) defines the structural conditions required for authority exercised during delivery to remain defensible when capital scrutiny accelerates.

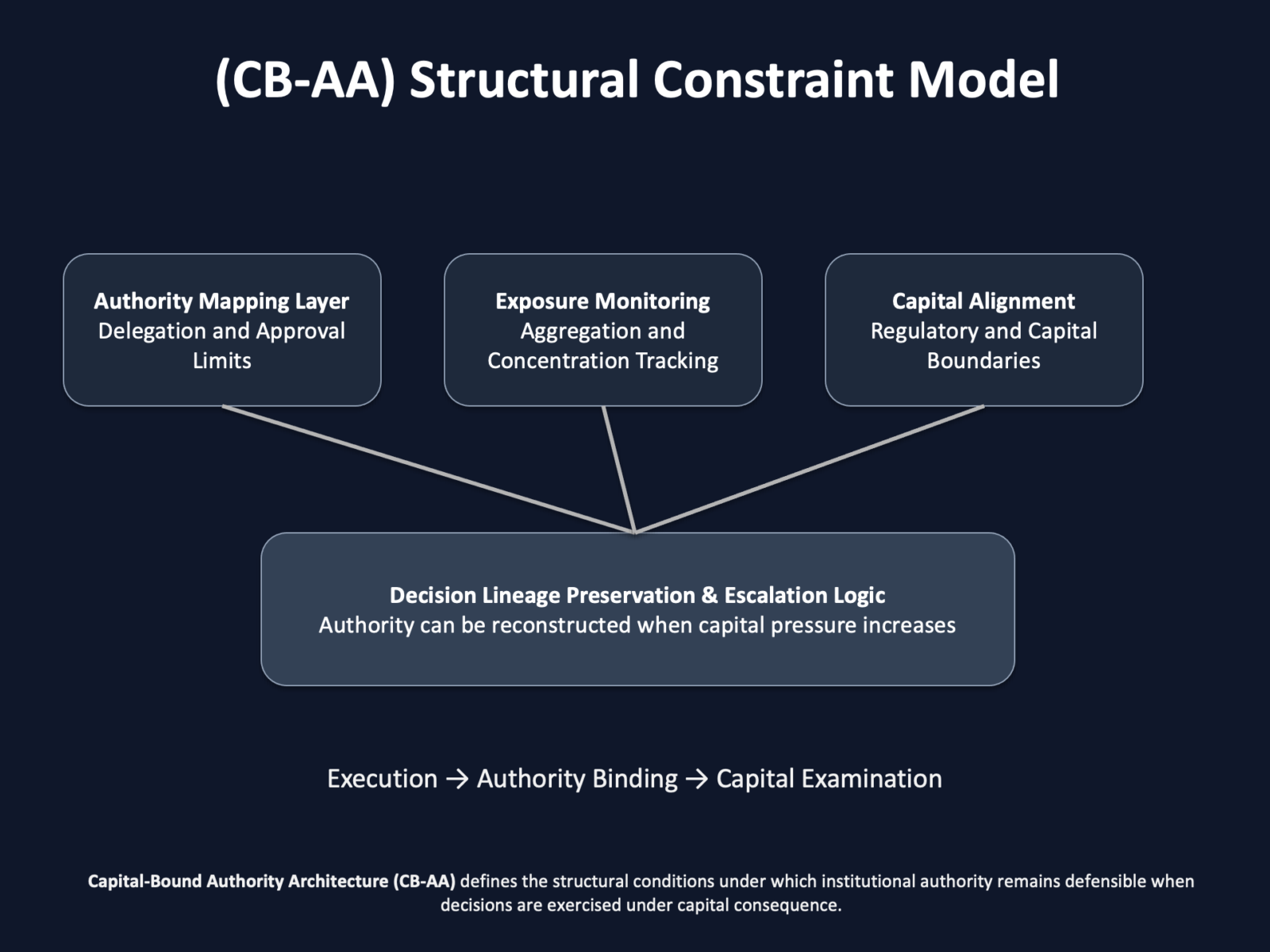

CB-AA defines how decision authority remains structurally bound to financial constraint across both formation and examination phases. The framework preserves authority lineage, aggregates exposure across reporting cycles, and ensures that decisions exercised during delivery remain reconstructable when capital scrutiny intensifies.

The CB-AA Standards specify the architectural requirements required for autonomous decision systems to preserve authority lineage, maintain policy state at execution, and prevent exposure migration across reporting cycles.

Authority is exercised once. Architecture determines whether it remains defensible when capital scrutiny accelerates.

Decisions are not examined when they are made, they are examined when they are inherited.

The Capital-Bound Authority Architecture defines the structural conditions that bind discretionary authority exercised during delivery to financial consequence under capital scrutiny.

Authority Binding Layer

Authority exercised during delivery appears operational in the moment. It becomes capital exposure later when financial consequence is reconstructed under scrutiny.

The Authority Binding Layer defines the institutional conditions that bind discretionary authority exercised during delivery to financial consequence under capital review.

Capital-Bound Authority Architecture defines those binding conditions.

- Execution Phase

- Authority Phase

- Examination Phase

Structured case records and authority reconstruction examples

Illustrative Exposure Formation and Reconstruction

Execution margin formation becomes visible when early operational decisions begin to shift financial sensitivity.

Authority drift, conditional completion, and delegated scope adjustments often converge at acceptance. When escalation thresholds are exercised without visibility into cumulative exposure, forecast margin can compress by two to six percentage points within active reporting cycles. This compression can occur without a single dispute or formal commercial trigger.

Execution-phase governance restores authority clarity before the compression embeds into cost.

Capital exposure reconstruction explains how institutions examine inherited decisions once capital scrutiny begins.

During lender diligence, insurance review, warranty enforcement, divestment analysis, or formal capital oversight, acceptance and delegation decisions are reconstructed against contractual authority and documented attribution.

Capital-stage governance determines whether financial exposure is defended, absorbed, transferred, or discounted.

Early Signals of Structural Drift

Structural drift develops through individually proportionate decisions that remain defensible in isolation but gradually reshape exposure across reporting cycles.

Early signals often appear when conditional acceptance volume increases, when delegated approvals cluster near authority limits, or when reconstruction of earlier decisions begins to rely on narrative interpretation rather than preserved decision state.

When these signals appear, the question is no longer operational performance. It becomes whether authority exercised during delivery will remain defensible when capital scrutiny intensifies.

Illustration: Structural Drift During Execution

During a multi-package infrastructure upgrade approaching commissioning, several mechanical and electrical scopes were accepted with conditions to preserve delivery sequence. Each adjustment appeared minor and remained within delegated approval limits. No individual decision triggered escalation, and delivery continued without interruption.

Across several reporting cycles, forecast margin moved from 12.5 percent to approximately 9.4 percent. There was no dispute, no claim process, and no commercial event signaling instability. The compression formed within accepted work rather than through an explicit breach.

Later reconstruction of the acceptance record revealed a different pattern. Conditional approvals had been exercised repeatedly, but their financial effect had never been evaluated collectively. Each decision was defensible in isolation. Aggregated across scopes, the approvals absorbed scope into the commercial position and increased financial sensitivity.

Escalation discipline was reinforced while delivery continued, and further compression was halted before close-out positioning hardened. The project stabilized without dispute because authority boundaries were recalibrated before capital scrutiny intensified.

Individually proportionate decisions can reshape financial exposure when authority is exercised without a structure that aggregates their effect.

Execution decisions shape financial exposure long before scrutiny begins.

Architecture determines whether those decisions remain attributable when institutions reconstruct them.

The control point where execution binds financial responsibility.

The determination layer where binding decisions are reconstructed under capital scrutiny.

Deployment-Grade Instruments

Institutional governance instruments deployed during live delivery engagements to preserve decision lineage, authority attribution, and exposure visibility across reporting cycles.

These instruments operate across execution formation and capital reconstruction phases.

Engagement windows

CB-AA engagements occur when discretionary authority begins to accumulate exposure before formal capital scrutiny emerges.

• During emerging execution-phase margin compression

• Prior to refinancing or transaction milestones

• When conditional acceptance volume is increasing

• Before insurance or audit review formalizes

• During active insurance, warranty, lender, or audit review when acceptance authority must be reconstructed against contractual and documented attribution

Where scrutiny has already begun, the focus shifts from prevention to defense.

→ Engage