Decision Authority Governance

Where Capital Consequence Is Determined

When projects enter claim review, refinancing, audit inquiry, or divestment diligence, the focus shifts from physical completion to financial interpretation. The question is no longer whether the work was delivered, but whether the decisions that bound financial responsibility can be reconstructed with clear authority, documented attribution, and commercial alignment.

Decision authority provides the structure that determines whether exposure can be defended under scrutiny or whether valuation tolerance begins to narrow in response to uncertainty.

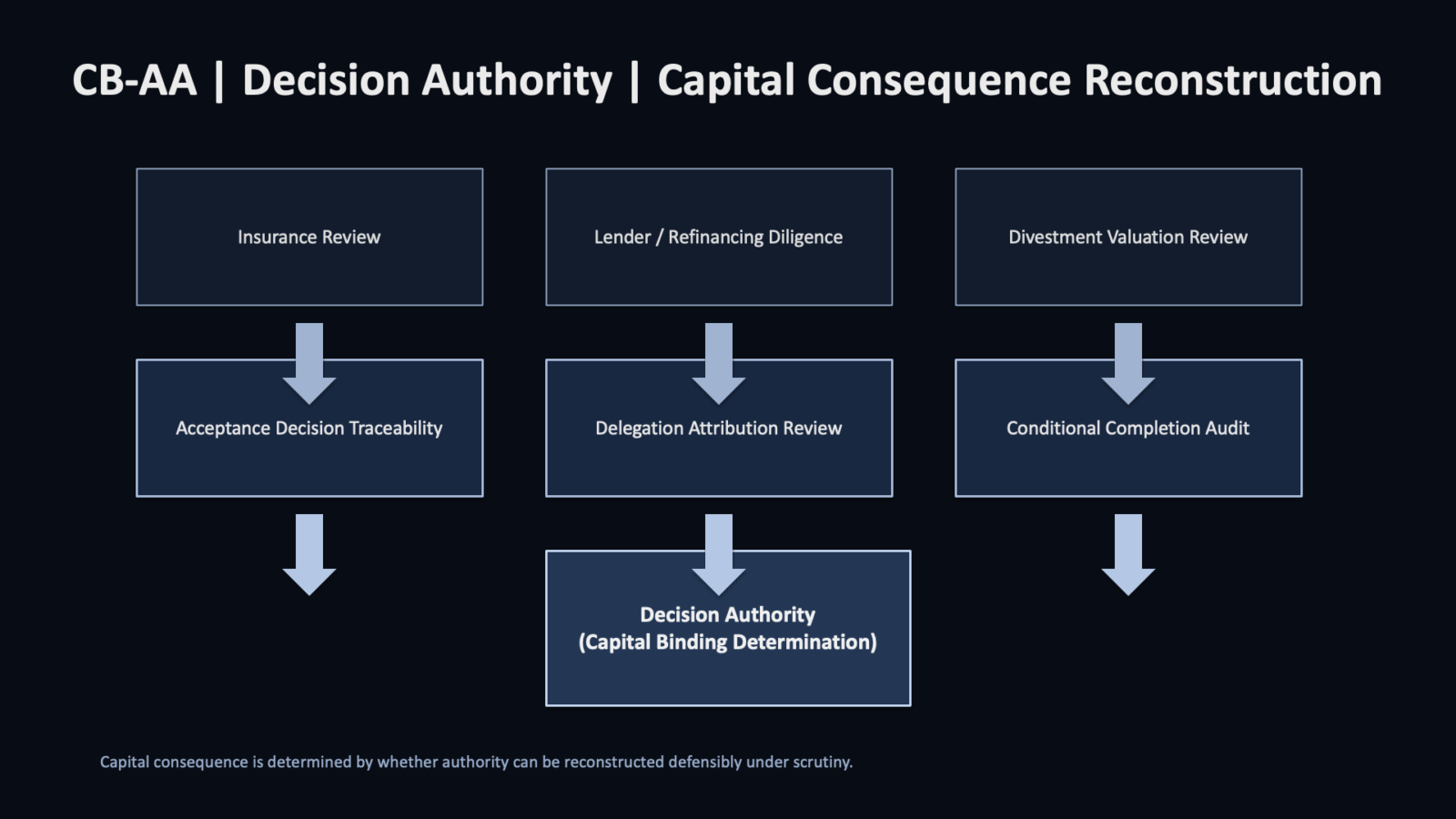

The CB-AA Decision Authority structure illustrates how external capital scrutiny converges on acceptance records, delegated approvals, and conditional completion decisions to determine whether financial responsibility remains defensible.

Decision authority determines whether acceptance decisions made during execution remain defensible when examined under external capital scrutiny.

Decision authority governs:

• Who exercised binding approval

• Under what contractual threshold

• With what documented commercial attribution

• Under which conditional boundaries

• And whether escalation discipline was preserved

During execution, these questions can feel procedural. Under capital scrutiny, they become determinative.

Capital Exposure Example

Operational Trigger

During refinancing of an energy asset delivered under schedule pressure, lender due diligence extended beyond operational performance to examine retained obligations and the structure of conditional acceptance exercised during execution.

Authority Condition

Conditional approvals had been exercised within delegated limits and no formal escalation had been triggered. Responsibility formed incrementally through cumulative acceptance decisions rather than through a single contractual breach.

Under capital scrutiny, reconstruction of the acceptance record revealed uneven commercial attribution across cumulative approvals. Delegation thresholds had been applied individually without consolidated exposure mapping.

Financial Consequence

Valuation sensitivity modeling linked the margin movement to authority ambiguity rather than performance deficiency. The lender’s financial interpretation therefore depended on whether decision authority could be reconstructed clearly across acceptance events and delegated approvals.

Decision authority is exercised through reconstruction.

Reconstruction traces:

• Acceptance events

• Delegated approvals

• Conditional completions

• Escalation decisions

• Commercial reservations

• Authority thresholds under contract

The purpose is not historical review. It is exposure stabilization while consequence is still manageable.

When reconstruction is possible, exposure can be contained.

When it is not, consequence hardens.

Execution Margin Formation reflects what happens in practice as delivery unfolds and exposure begins to take shape. Conditional approvals are exercised, delegated limits are applied, and cost becomes bound in real time while work continues.

Decision authority becomes visible later, when those same approvals are revisited under refinancing, insurance review, audit inquiry, or divestment diligence. It governs whether the financial commitments created during execution can withstand capital examination.

Acceptance authority is where cost is committed in the moment. Decision authority determines whether that commitment remains defensible when examined.

Capital consequence rarely arises solely from operational underperformance. It materializes when authority discipline cannot be clearly demonstrated under review.

During insurance assessment, it shapes claim survivability and recovery position. Within lender diligence, it narrows or preserves valuation tolerance. Throughout divestment review, it affects retained liability exposure. Under audit inquiry, it defines accountability for attribution.

Decision authority provides the structural framework that determines whether financial consequence is absorbed internally, transferred contractually, defended under scrutiny, or reflected as a valuation adjustment.

Engagement Window

Engagement is most effective when:

• Conditional acceptance volume is increasing

• Delegation thresholds are unclear

• Close-out reconciliation is widening

• Refinancing or transaction timing is approaching

• Insurance scrutiny is anticipated

→ Engage